All

That Glitters Is Not Gold By VITO J. RANCANELLI

- April 13, 2009

Tanzanian

Royalty rallied on the reputation of CEO James Sinclair. But

the gold guru's actions cast doubt on the exploration company's

fortunes.

GOLD EXPLORER TANZANIAN ROYALTY

EXPLORATION HAS NO revenue, no earnings and no proven gold,

as well as some accounting issues. So why do its shares trade

at a premium to peers that seem to be in much better shape?

It helps that its chairman and chief executive,

James E. Sinclair, is famous for correctly forecasting gold

prices, and he is very bullish on the metal on his avidly

followed newsletter-style Website, www.jsmineset.com. Over

the years, Sinclair's views on gold have been sought out by

newspapers like the New York Times and on cable-TV networks

like CNN. Barron's has interviewed him and run his advertising.

Jim Sinclair, shown on the U.S. Rare Coin

Investments Website, is bullish on gold prices. He expects

them to rise to about $1,650 an ounce by 2011.

So it is surprising to learn

that the widely known bull on gold has been a steady seller

of shares of his own gold-related company.

Tanzanian Royalty (ticker: TRE) is a

small-cap Canadian outfit (including its predecessor)

that has been looking for gold for a decade. None of

its properties, all in Tanzania, have yet shown economically

viable mineral reserves, as defined by regulators. Were

it valued more like rivals with similar cash and gold

reserves, its share price would be substantially lower

than the current $4.05.

TRE's market capitalization is $370

million. Some rival miners with more cash on their balance

sheets than TRE and actual gold have market caps one-sixth

that size.

Dubbed Mr. Gold by the media for prescient

calls on gold in the late 1970s and 1980s, Sinclair ran his

own precious-metals trading firm in those days. On his Website

and in interviews, a bullish Sinclair today says gold will

trade as high as $1,650 an ounce by January 2011 and says

he would wager $1 million that it will. Gold was trading at

about $881 an ounce Friday.

In an interview with Barron's last week, Sinclair

disputed the view of TRE's shares as overvalued, saying the

market cap was due to its less-capital-intensive structure

and the potential of its properties. Moreover, he promised

that a third-party evaluation of its important Kigosi property

in Tanzania would be ready in "about six months."

While TRE puts out press releases on his share

purchases, the CEO says he isn't required to put out press

releases on his share sales.

In addition to Sinclair's devoted following

-- he is sometimes referred to as "Uncle Jim" on

Yahoo!'s TRE message boards -- shareholders could be speculating

that he will sell TRE to a big miner. Though he was ousted

as chairman of Sutton Resources in 1995, some remember that

Sutton was bought by Canadian gold giant Barrick Gold (ABX)

in April 1999 for its Tanzanian properties. Not everyone credits

Sinclair for the deal, but some do.

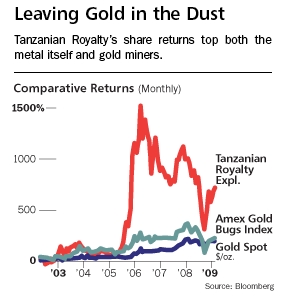

There is no question that Tanzanian shares

have done extremely well since Sinclair and his family became

its largest stockholders in April of 2002 (as a result of

a merger they ended up with about 25% of the shares, which

trade on the American Stock Exchange, and on the Toronto Stock

Exchange under the ticker TNX.Canada). TRE shares have soared

about 711% since then. That trounces the 218% rise in the

metal itself over the same period, though TRE has no gold

reserves. Meanwhile, the American Stock Exchange Gold Bugs

Index (HUI) composed of companies involved in gold mining

-- many of which have gold in hand -- is up much less, just

198%. Since last summer, the credit crisis has hurt the juniors,

as the small prospectors are called, on worries that they

won't be able to get the financing needed to develop mines.

In that time, TRE has fallen less than its peers.

Yet TRE faces the same business risks that

rivals do, and continued financing is among the most important.

TRE's financing is accomplished by the unusual method of private

placements of its stock with CEO Sinclair, who then sells

his shares into the market.

In a March 5 press release on this subject

from the company, TRE reported that Sinclair has purchased

another 189,036 shares for one million Canadian dollars (US$810,000)

and that Sinclair's "total share placements to date aggregate

C$22 million." TRE doesn't put out releases on his sales

of millions of shares of the stock, though he has steadily

sold TRE shares into the open market. He sold stock more than

50 times in 2008. Over the years, as the stock price soared,

Sinclair and his family have reduced their TRE stake from

25% in 2002 to less than 3% now, company documents show. According

to Canada's System for Electronic Disclosure by Insiders,

or SEDI, his TRE stake has dropped to about 2.3 million shares

as of March 12, from 3.9 million in October 2004.

Though company announcements claim he is financing

TRE, ultimately the main financiers are mostly the retail

shareholders who buy from Sinclair. In his interview, he repeated

that he is a strong backer of the company and that he recently

agreed to another $2.43 million private placement for TRE

shares. But if Sinclair is unwilling or unable, for any reason,

to continue these private placements, how will TRE finance

its activities? With the credit crunch, the environment has

become tougher for juniors dealing in speculative endeavors

to get traditional financing through selling equity directly

into the stock market. That is especially true for a company

without any proven reserves, like TRE.

When

Barron's asked why he was selling TRE shares, Sinclair replied

that it was for personal liquidity. Asked why he didn't put

out a press release on the stock sales, Sinclair replied,

"Is it required?...I take no salary, no options, no warrants.

I have purchased more than I have sold." But when asked

to furnish that data, he refused and referred Barron's to

the SEDI Website. The selling trend shown by SEDI insider-trading

records is seconded by TRE documents: Sinclair had 3.17 million

shares in August 2008 and 2.88 million in January.

Sinclair has declared he won't go to the public

markets to finance the company, but it is probable that TRE

couldn't easily get an investment bank to underwrite its shares

because of that lack of economically viable mineral resources.

There is little institutional interest --

roughly 17% of TRE's 89 million shares are held by mutual

funds, according to Bloomberg. TRE filings report that 83%

of its shareholders are American, most of them individual

shareholders who, unless they are familiar with Canada's SEDI,

are perhaps unaware that Sinclair is selling shares after

buying them.

These TRE shareholders might not know that

Sinclair is listed as a "disciplined person" on

the Website of the Canadian Securities Administrators, an

organization of provincial securities regulators. On July

22, 1998, Sinclair was ordered by the British Columbia Securities

Commission to pay $2,000 to settle a violation of "misrepresentation"

in a press release having to do with Sutton. Sinclair called

it a small "misunderstanding."

Unlike many peers, TRE doesn't appear to be

followed by any sell-side analysts from brokers specializing

in Canadian miners, so third-party information is scarce.

TRE is an Alberta-registered corporation with headquarters

in South Surrey, B.C., while Sinclair himself is based in

Sharon, Conn.

If analysts looked at TRE, they would find

its finances are stretched. For example, as of Nov. 30, the

company had about $1.2 million in cash, not much more than

the $1.17 million in salaries and fees paid to its directors

for the fiscal year ended Aug. 31, 2008.

As Sinclair makes clear, TRE is a royalty

company, not a mining firm. That means it will find lands

with potential, then sell them off to bigger miners in exchange

for royalties from mine production, if that occurs. As Sinclair

noted, royalty firms need less capital than a junior miner,

but $1.2 million is hardly enough. Even royalty firms must

drill on properties to entice partners.

According to a TRE filing for the year ended

last Aug. 31, TRE spent $2.37 million for exploration in fiscal

2008, just $267,000 more than fiscal 2007. For the past three

years TRE has spent less than $8 million in exploration and

written off roughly half of that in mineral-property value.

By comparison, Barrick eventually spent some $400 million

to develop its Buzwagi mine in Tanzania.

On its Website's projects-description page,

TRE often promotes its own properties in Tanzania that are

near Barrick developments and continues to list Barrick as

a joint-venture partner in an Itetemia prospect. Barrick says

it has no JV partnership with TRE.

Sinclair disputes that TRE doesn't have the

cash for its drilling program: "We have our own drills

and team." Sinclair also said the firm has one rig for

all its properties, similar to some other companies. None

of them, however, has the market cap of TRE.

Moreover, David Duval, a Vancouver-based mining

technologist, says that before a gold mine can be developed,

$20 million to $30 million in drilling and exploration costs

are typical, depending on the property. Duval called Barron's,

saying he had done so at the behest of Sinclair and that he

is a consultant to TRE. Duval is also listed as a contributor

and co-founder of Sinclair's Website: www.jsmineset.com.

Something else that might trouble investors

is that TRE has been cited by its auditor KPMG for a "pervasive

material weakness" in accounting controls. In TRE's annual

report for the year ended last Aug. 31, KPMG, gave an adverse

opinion on the effectiveness of TRE's internal controls: "The

company has limited accounting personnel with expertise in

generally accepted accounting principles to enable effective

segregation of duties with respect to financial reporting

matters and internal control over financial reporting."

The company says it is attending to that.

But the greatest risk to TRE shareholders

is its lack of gold reserves. TRE has put out many positive-sounding

press releases since 2002 about its properties, but it hasn't

discovered any economically viable gold resources as defined

by a National Instrument 43-101-compliant document. The document

-- established by Canadian authorities after the giant BRE-X

Minerals fraud in 1997 -- is an officially sanctioned disclosure

measure of "mineralization," or the presence of

minerals like gold.

An NI 43-101 reports whether the property

has "proven" minerals -- the highest measure of

geological confidence -- or lesser reliability, like "probable,"

or "inferred," the least strong. No miner is likely

to get substantial mine-development financing without such

a document, and TRE doesn't have one.

Instead, press releases are issued about preliminary

drilling results, but no gold mines follow. For example, TRE

reported Oct. 13, 2004, a "significant gold discovery"

in the Luhala property in the Lake Victoria Goldfields area.

On Oct. 19, 2005, another "significant gold discovery"

was announced in the Tulawaka region. Three to four years

later, there is no news of any commitments to develop these

properties into gold mines, or any of Tanzanian's leaseholds.

Sinclair is upbeat about TRE's probability

of finding economically viable gold soon: "We have discovered

about four grams per ton in Kigosi....We are going to have

an NI 43-101 on Kigosi in about six months -- as soon as consultants

finish their work," he says. "It could fall apart...[BUT]if

all goes well, from the time the report is completed there

will be a mine within 18 to 24 months."

"All of our extremely positive results

are on the Website. If gravels continue to show the grades

that are indicated now, I would move immediately to an open

pit and underground mine," Sinclair vows.

That sounds optimistic, since gold mines often

take three or more years to build after the finding of economically

viable metal.

Despite having resource prospects that don't

measure up to peers', TRE's valuation is golden compared with

many. (See nearby table.) For example, TRE has its $1.2 million

in cash, no gold reserves and its $370 million market cap.

Meanwhile, rival MDN (MDN) whose market cap is $55 million,

also has prospects in Africa, but $14.6 million in cash and

100,000 ounces of gold resources, according to broker Canaccord

Adams. Semafo (SMF) has a market cap similar to TRE's but

also has 4.8 million ounces of gold reserves.

Another way to benchmark TRE is to look at

the S&P/TSX Metals & Mining Index (STMETL) of 35 stocks,

many with real revenue and cash flow. The index's average

price/book ratio is 1.35, but TRE, which is in the index,

trades at about 17 times its book value of 24 cents a share.

Membership in such indexes and the International

Stock Exchange Gold index (HVY) may boost TRE shares higher

than they would be otherwise. In both indexes, TRE's weightings

are equivalent to companies with many times its market cap

and actual gold, like Eldorado Gold (EGO), which has 7.6 million

ounces of proven or probable gold.

Speaking with Barron's, Sinclair repeatedly

said that TRE's market cap is due to its less-capital-intensive

royalty structure and the value of its leaseholds. "It's

not me, it's the underlying assets. The company assets will

have to stand on their own two feet and I think that it can."

When it was pointed out that TRE has no NI 43-101, yet its

valuation was much higher than companies with 43-101- compliant

gold and actual gold, he replied: "I will come after

you," and ended the phone call.

Rising gold prices have boosted TRE's stock

value lately, but it needs to find some gold soon. Otherwise,

its exploration failures so far and its dependency on Sinclair's

financing methods will catch up with the shares.

While Sinclair has had success predicting

gold prices, TRE doesn't have a good track record of finding

gold in economically viable amounts. Without Sinclair, it

is likely TRE's market cap and share price would be significantly

less golden.

The Bottom Line If you apply the same metrics

to Tanzanian Royalty that are used for its peers, the stock

looks substantially overvalued. And Tanzanian has less cash

on its books than most.

When

Barron's asked why he was selling TRE shares, Sinclair replied

that it was for personal liquidity. Asked why he didn't put

out a press release on the stock sales, Sinclair replied,

"Is it required?...I take no salary, no options, no warrants.

I have purchased more than I have sold." But when asked

to furnish that data, he refused and referred Barron's to

the SEDI Website. The selling trend shown by SEDI insider-trading

records is seconded by TRE documents: Sinclair had 3.17 million

shares in August 2008 and 2.88 million in January.

When

Barron's asked why he was selling TRE shares, Sinclair replied

that it was for personal liquidity. Asked why he didn't put

out a press release on the stock sales, Sinclair replied,

"Is it required?...I take no salary, no options, no warrants.

I have purchased more than I have sold." But when asked

to furnish that data, he refused and referred Barron's to

the SEDI Website. The selling trend shown by SEDI insider-trading

records is seconded by TRE documents: Sinclair had 3.17 million

shares in August 2008 and 2.88 million in January.