Get On Board The Gold Train, Next Stop $1,800 By Scott Redler |

December 07, 2010

Gold has been one of the stories of the

market over the last several years as the global economic

crisis and an overall lack of trust in the “system”

has led investors to seek a more evergreen store of value.

I personally first began talking about Gold

in December 2008 when it was trading at $850/ounce. I felt

the technical indicators and a compelling story suggested

a move to $1,300-$1,500. Although I did not hold the SPDR

Gold Trust ETF (NYSE:GLD), which is my preferred vehicle

for trading gold, for that entire run, I traded gold on

several occasions within that time frame with much success.

When

you have a powerful idea, you must be able to execute it

in a way that fits in with your overall trading or investment

strategy, and that’s what I have done with gold. In

hindsight, do I wish I had bought tier four gold in 2008

after I made that prediction on CNBC, and held it for the

entire measured move? Sure, but I have not lost any sleep

over it. I feel content that I traded gold in a way I was

comfortable with. I have applied my own active, risk averse

approach to the gold trade, locking in gains and taking

risk off when it seemed appropriate to do so. Depending

on your overall strategy as a market participant, customize

your approach to trading gold.

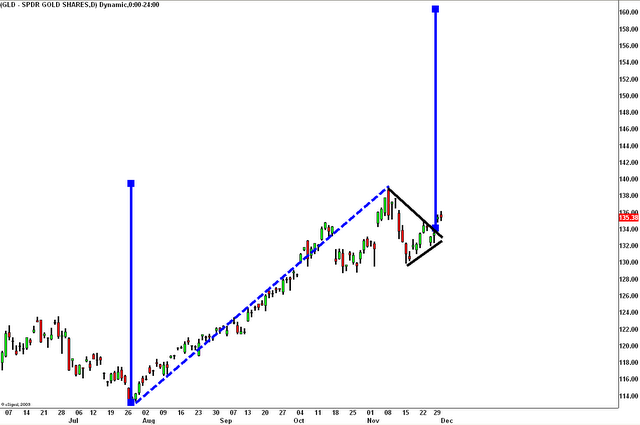

How the gold trade has evolved

While the basis for most of my trading decisions

comes from strict, prudent technical analysis, there has

also been a powerful story to tell about gold apart from

the charts.

Curtis Hesler told his readers to back up the truck and

buy Silver Wheaton (SLW) at $4 in late 2008 and Goldcorp

(GG) at $18. Sell here or buy a bunch more? Click here for

instant access to updates in Professional Timing Service.

Over the course of the last several years,

the nature of the gold trade has evolved. Back in 2008,

when the price jumped from $850 to $1,000 an ounce, it was

the “fear trade.” Amid the global panic of the

credit crisis, investors wanted to own something tangible,

something they could touch and feel. Gold was seen a safe

haven.

Then, in 2009, the gold trade morphed into

the “inflation trade” as the world recovered

from the depths of the historic recession, as I noted on

CNBC in September 2009. As governments raced in to save

the day and print money to rescue institutions, investors

feared the implications of the newly minted “too big

to fail” paradigm. During that time, the reverse head

and shoulders pattern formed, sending spot gold from $1,000

to $1,224/ounce.

In 2010, gold shape-shifted once again into

the “sovereign debt trade.” Fears of contagion

in the Eurozone debt crisis have engendered calls for the

end of the Euro and even the European Union. As the year

has gone on, the crisis has worsened. Ireland recently joined

Greece as the first PIIGS to require a massive bailout.

Doubts about the future of the Euro have sent gold from

$1,265 to as high as $1,400+ an ounce.

Where are we now?

Now,

with 2010 getting closer to the rear view mirror, it’s

time to start looking forward to the next leg of the journey.

What will gold look like in 2011 and beyond? Well, all indications

are that the European sovereign debt crisis will get worse

before it gets better. A massive bailout for Portugal seems

almost inevitable at this point, and then we start getting

into the real big kids on the block. A bailout for Spain,

the ninth largest economy in the world, might require more

money that the system could tolerate. If a domino of that

size were to fall, who knows what could be next to follow?

Many people judge “bubbles”

and over-hyped phenomena in the financial world based on

when the retail public take notice en masse. Conventional

wisdom now says that when the retail public starts hearing

the story and jumping on the bandwagon, a top is imminent.

With cash for gold ads polluting our television screens,

gold vending machines popping up around the country, and

gold stories starting to populate the covers of mainstream

magazines, it certainly feels like the gold story fits the

bill. However, it would be fallacious to blindly judge something

only on such a basic level without digging deeper. Each

case study, when you are presented with a framework, must

be reasoned based on its own merits. In this instance, I

believe the facts supporting another surge higher in gold

prices outweigh the doubts accompanying this analogy.

There is no substitute for the real

thing. The equity market rally could be fool’s gold.

Even without the worst case scenario coming

to fruition, gold seems destined to go higher as long as

fear remains a part of the equation. Over the last couple

months, as the market trudged ever higher, we were lulled

into a sense of complacency. The market, once ruled by headline

risk and overnight moves, had become more focused on earnings

and valuations, but that doesn’t mean things couldn’t

return to what they used to be.

The rosy complexion of the market was driven

largely by expectations that the Fed would prop up asset

prices at every turn, and it could be argued that prices

are artificially inflated at current levels. The Fed has

taken a “fake it until you make it” approach;

continue to prop up asset prices until the economy picks

up. If it doesn’t work, at what point are QE3, QE4

and QE5 no longer an option? Over the last week or so we

have seen headlines reassert their power, with the Ireland

debacle and the Korea skirmish serving as a stark reminder

of what can happen. Tinkering with asset prices causes price

instability, and investors will not be so quick to fall

into the same old trap.

Inflation: There is also

the giant elephant in the room: inflation. Many argue that

we are currently in a strictly deflationary environment

that needs to be fought at all costs, and that if real inflation

does appear, the Fed has tools to fight it. Government officials

still claim there is no inflation, but as food and gas prices

skyrocket around the world, consumers are scratching their

heads over such an assertion. We have also seen “shadow

inflation”, which can be understood as value deflation.

Instead, for example, of getting a 7-ounce bag of coffee

beans at Wal-Mart, you can now only get 6-ounce bag that

costs the same price, a fact that is not taken into account

in the Consumer Price Index (CPI). While a gym is cutting

costs or keeping fees stable, for example, they are getting

rid of water fountains and turning off the air conditioning.

In general, the average investor has grown skeptical of

our already discredited leadership.

Nassim

Taleb, a renowned expert on understanding black swans and

left tail risk, describes the potential hyperinflation phenomenon

as trying to get ketchup out of the bottle. Upon the first

couple of smacks, little-to-nothing might come out. Smack

the bottom of the bottle three or four more times, though,

and the whole contents might end up on your plate. The Fed’s

QE program is arguably the biggest science experiment of

all-time, performed with taxpayer money, and the end result

is unclear. Even Ben Bernanke admits that he does not know

what the outcome will be given the complexity and ground-breaking

nature of his Fed’s bold actions. For all we or they

know, all this money printing and monetization of debt could

be setting the stage for a period of high and difficult-to-fight

inflation. It remains to be seen whether, at that stage,

the Fed would have the credibility or the tools to combat

runaway prices.

All Likely Scenarios Point to Higher

Gold Prices

If all-out disaster can be averted in Europe,

and the U.S. economy can continue to grow, gold can still

see a slow technical grind to $1,600-$1,800. If Europe starts

to falter even more (remember, debts come due over the next

several years), which seems likely at this point, gold can

really go parabolic to $2000+. We are heading toward an

environment in which nobody feels comfortable holding any

fiat currency.

Gold, something that cannot be conjured

out of thin air and has universally recognized value, would

be seen as the primary store of value. Other precious metals

like silver, which has outperformed gold handily this year,

would likely behave in a similar fashion. The U.S. mint

has seen a dramatic rise in demand for silver eagle coins,

with sales up 30% since 2007.

The two most likely scenarios for the world

economy both offer strong support for higher gold prices.

Further deterioration in Europe and the US would trigger

an exodus from fiat currencies into gold, and a high-inflation

recovery would send gold prices soaring. Gold is both a

safe-haven play and an inflation hedge. The only scenario

where gold could burst like a bubble is if, against all

odds, the economy recovers, budget deficits self-correct

as aggregate demand and tax revenues soar, the Fed is able

step in to stem the tide of high inflation at just the right

time and the world presses on into the 21st century like

this little recession never happened. Sorry folks, but I

just don’t see that happening.

State Debt Crises: The Story of

CAIN and (Un)Abel

In Europe, they were able to come up with

a clever moniker, PIIGS, to succinctly represent the most

boorish animals on the farm, and its only appropriate the

for us Americans to come up with our own distinction as

state budget crises becomes more pressing.

I

am going to call it the story of CAIN and (Un)Abel. CAIN

represents seven of the most rotten pillars of our union,

the states with the most urgent budget concerns–C

(California), A (Arizona, Alaska), I (Illinois), N (New

York, New Jersey)–while (Un)Abel describes the country

as a whole. (Un)Abel, as in unable to do anything about

the impending crisies. Given the current political climate

and implicit anti-bailout mandate of the new Congress, the

Federal government might be powerless to do anything but

accept painful state defaults. Before we know it, we could

all be ancestors of evil.

In April, Congress plans to meet to discuss

debt levels, which will include how to deal with individual

state crises. Keep in mind, this is the same Congress that

has been recently restocked with (supposedly) debt-conscious

Republicans who will (presumably) feel obligated to put

their foot down on further massive government spending.

The possibility of further deficit spending appears remote,

if not dead-as-a-doornail. It just so happens that 2011

could be the year that CAIN starts to face some serious

trouble, and may need some serious help to avoid killing

his brother (Un)Abel.

If large state dominoes start to fall and

creditors are forced to the table, it could lead to rehashing

of the widespread fears from 2008. California, after all,

is the fifth largest economy in the world, and would be

a mighty large domino. The non-partisan Legislative Analyst’s

Office projected on November 10th that the budget shortfall

in California will be $25.4 billion, twice as large as state

political leaders had predicted and more than a fifth of

the general fund. A default by a sovereign state (and it’s

biggest, at that) would affect the credit rating of the

United States as a whole. A bailout, if it were approved,

with deep cuts for pension holders and other programs would

likely be met with angry demonstrations by Californians,

much like we have seen in Greece, Ireland and across Europe.

Civil unrest would do wonders for the price of gold. As

Chris Whalen stated earlier this month, this entire situation

amounts to a Federalist crisis for the United States. These

issues are not limited to California.

What to do with gold

Gold has a compelling long-term story for

higher prices, but what is the best way to approach the

trade? For an active approach, you could be long tier one

here versus current support of $1,310-1,330, which would

be the technical stop-loss on the trade. If nothing else,

investors should consider having gold and/or other precious

metals as a portion of their portfolio as a risk protection

against the possibility of further deterioration of the

world economy and high future inflation. We will be looking

for more calculated technical areas to potentially add further

tiers of gold for the next macro move.

When

you have a powerful idea, you must be able to execute it

in a way that fits in with your overall trading or investment

strategy, and that’s what I have done with gold. In

hindsight, do I wish I had bought tier four gold in 2008

after I made that prediction on CNBC, and held it for the

entire measured move? Sure, but I have not lost any sleep

over it. I feel content that I traded gold in a way I was

comfortable with. I have applied my own active, risk averse

approach to the gold trade, locking in gains and taking

risk off when it seemed appropriate to do so. Depending

on your overall strategy as a market participant, customize

your approach to trading gold.

When

you have a powerful idea, you must be able to execute it

in a way that fits in with your overall trading or investment

strategy, and that’s what I have done with gold. In

hindsight, do I wish I had bought tier four gold in 2008

after I made that prediction on CNBC, and held it for the

entire measured move? Sure, but I have not lost any sleep

over it. I feel content that I traded gold in a way I was

comfortable with. I have applied my own active, risk averse

approach to the gold trade, locking in gains and taking

risk off when it seemed appropriate to do so. Depending

on your overall strategy as a market participant, customize

your approach to trading gold. Now,

with 2010 getting closer to the rear view mirror, it’s

time to start looking forward to the next leg of the journey.

What will gold look like in 2011 and beyond? Well, all indications

are that the European sovereign debt crisis will get worse

before it gets better. A massive bailout for Portugal seems

almost inevitable at this point, and then we start getting

into the real big kids on the block. A bailout for Spain,

the ninth largest economy in the world, might require more

money that the system could tolerate. If a domino of that

size were to fall, who knows what could be next to follow?

Now,

with 2010 getting closer to the rear view mirror, it’s

time to start looking forward to the next leg of the journey.

What will gold look like in 2011 and beyond? Well, all indications

are that the European sovereign debt crisis will get worse

before it gets better. A massive bailout for Portugal seems

almost inevitable at this point, and then we start getting

into the real big kids on the block. A bailout for Spain,

the ninth largest economy in the world, might require more

money that the system could tolerate. If a domino of that

size were to fall, who knows what could be next to follow? Nassim

Taleb, a renowned expert on understanding black swans and

left tail risk, describes the potential hyperinflation phenomenon

as trying to get ketchup out of the bottle. Upon the first

couple of smacks, little-to-nothing might come out. Smack

the bottom of the bottle three or four more times, though,

and the whole contents might end up on your plate. The Fed’s

QE program is arguably the biggest science experiment of

all-time, performed with taxpayer money, and the end result

is unclear. Even Ben Bernanke admits that he does not know

what the outcome will be given the complexity and ground-breaking

nature of his Fed’s bold actions. For all we or they

know, all this money printing and monetization of debt could

be setting the stage for a period of high and difficult-to-fight

inflation. It remains to be seen whether, at that stage,

the Fed would have the credibility or the tools to combat

runaway prices.

Nassim

Taleb, a renowned expert on understanding black swans and

left tail risk, describes the potential hyperinflation phenomenon

as trying to get ketchup out of the bottle. Upon the first

couple of smacks, little-to-nothing might come out. Smack

the bottom of the bottle three or four more times, though,

and the whole contents might end up on your plate. The Fed’s

QE program is arguably the biggest science experiment of

all-time, performed with taxpayer money, and the end result

is unclear. Even Ben Bernanke admits that he does not know

what the outcome will be given the complexity and ground-breaking

nature of his Fed’s bold actions. For all we or they

know, all this money printing and monetization of debt could

be setting the stage for a period of high and difficult-to-fight

inflation. It remains to be seen whether, at that stage,

the Fed would have the credibility or the tools to combat

runaway prices. I

am going to call it the story of CAIN and (Un)Abel. CAIN

represents seven of the most rotten pillars of our union,

the states with the most urgent budget concerns–C

(California), A (Arizona, Alaska), I (Illinois), N (New

York, New Jersey)–while (Un)Abel describes the country

as a whole. (Un)Abel, as in unable to do anything about

the impending crisies. Given the current political climate

and implicit anti-bailout mandate of the new Congress, the

Federal government might be powerless to do anything but

accept painful state defaults. Before we know it, we could

all be ancestors of evil.

I

am going to call it the story of CAIN and (Un)Abel. CAIN

represents seven of the most rotten pillars of our union,

the states with the most urgent budget concerns–C

(California), A (Arizona, Alaska), I (Illinois), N (New

York, New Jersey)–while (Un)Abel describes the country

as a whole. (Un)Abel, as in unable to do anything about

the impending crisies. Given the current political climate

and implicit anti-bailout mandate of the new Congress, the

Federal government might be powerless to do anything but

accept painful state defaults. Before we know it, we could

all be ancestors of evil.