Investing

Gold, Again, Becomes a Shield Against the Unknown

By CONRAD DE AENLLE Published: September 23, 2007

GOLD

is supposed to be a destination for scared money, but as the

credit crunch intensified last month, this presumed haven

lost value along with many other assets. Only after the worst

of the crisis had passed did traders return to gold, sending

its price sharply higher.

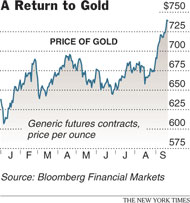

The metal has gained about $80 an ounce, or

12 percent, since mid-August, around the time the stock market

reached a trough. While share prices have since had ups and

downs, gold's ascent has been nearly uninterrupted.

This strength

heralds further gains for physical gold and for shares

of mining companies, many analysts and fund managers

predict. They offer a variety of reasons, ranging from

a desire to hedge against a falling dollar, a weaker

economy or geopolitical instability, to a conventional,

Econ 101 imbalance of supply and demand.

The bullish consensus, and the abundance of factors

invoked in reaching it, result from an oddity of the

gold market: it thrives on uncertainty, and investors,

even authorities on commodities, are uncertain what

makes it tick.

“What is unsatisfying about gold

is that there is no single easy explanation for why

it moves either up or down,” said Fred Sturm,

manager of the Ivy Global Natural Resources fund. “There

are a number of elements that impact the price direction.”

Stuart Schweitzer, global market strategist

at JPMorgan Private Bank, is another who finds gold a head-scratcher.

“If there’s a rule where gold

is concerned, it’s that it doesn’t trade predictably,”

he said.

That was the case last month, when gold failed

to rise along with anxiety about the availability of credit,

as might have been expected. Instead, it fell about $50 an

ounce from late July to mid-August, a result of selling by

hedge fund managers.

Gold is an asset coveted as a hedge against

risk, but these mostly unregulated and highly leveraged funds

acquired large positions, using the substance as a tool for

speculation. When other markets on which they had made big

bets turned bad — subprime mortgages, for instance —

the funds were forced to sell gold, among other holdings,

to raise cash.

“There has been a lot more leveraged

money in gold over the past few years, compared to history,”

Tony Lesiak, a gold analyst for UBS, said in a note to the

bank’s clients. “So when we get financial market

risk aversion, the same investors who are cutting long equity,

long credit and long emerging-market positions also cut back

on gold.”

Now that hedge fund selling has abated, a

serious impediment to higher gold prices has been removed,

advisers contend. Another reason to expect further gains,

even with gold now at $731.50 an ounce, close to its highest

price since 1980, they say, is that little further supply

is likely to come to the market.

Central banks, mainly in Western Europe, have

been selling gold from their reserves as they diversify into

other assets, and are thought to be nearly done with those

sales. Supplies from mines rose a mere 3 percent last year,

while another usual source of supply, scrap, fell 27 percent.

There is plenty of demand, meanwhile, from

the flourishing middle classes in China and India and, says

John Hathaway, manager of the Tocqueville Gold fund, from

central banks in countries that have enjoyed gains from foreign

trade, like Russia, the Persian Gulf states and, again, China.

Then there is the risk-aversion play. Hedge

fund sales masked demand that might have arisen in the subprime

crisis, but analysts expect a demonstrable resumption of flights

to safety if the dollar keeps falling, credit conditions worsen,

political hot spots ignite or if some other bad event occurs

that they can’t yet envision.

Gold is “an asset that people want to

own as protection for risks they can’t really analyze

and get their arms around,” said Mr. Schweitzer at JPMorgan.

“That risk has gone up.”

If investors buy the arguments for gold, they

must then decide how to buy access to it. They can acquire

the physical metal, but that entails costs for storage to

guard against theft and the hidden cost of holding an asset

that does not pay interest or dividends.

A way to mitigate the first expense is to

buy an exchange-traded fund like the StreetTracks Gold Trust,

the largest of several E.T.F.’s on the New York Stock

Exchange that hold bullion in quantity so that storage costs

are spread thin.

The main alternative to physical gold is shares

of mining companies. They have failed to keep pace with bullion

over the last year, and fund managers and analysts have no

trouble explaining why. As Mr. Sturm summarized it, gold mining

“is a pretty lousy business.”

The costs of energy and the chemicals used

in mining tend to rise along with the metal, so company profits

are prone to rise more slowly than the price of gold, he noted.

That makes gold one of the less-rewarding substances to produce

during a commodities boom.

“Very few gold producers are beating

their chests, bragging about how much free cash they’re

generating,” Mr. Sturm said.

Though he finds gold mining “a tough

gig,” his expectation of higher gold prices and lower

input costs has led him to increase holdings of mining stocks.

He tends to favor companies with mines in politically stable

countries and with enough ore in their reserves that it would

take a decade or more to extract it all.

His favorite example is Gold Fields in South

Africa. Its stock became very cheap, in his view, as its price

fell from $26 in the spring of 2006 to $14 last month as the

price of bullion showed little net change.

Mr. Sturm’s eclectic list of choices

includes Agnico-Eagle Mines, a smaller Canadian company that

he expects “will probably have some brand-spanking-new

gold reserves coming at a time of rising prices.” For

investors interested in mixing their metals, he likes Impala

Platinum in South Africa and Silver Wheaton, an American company

that provides financing for silver mines around the world

in exchange for interest and royalty payments.

Echoing Mr. Sturm’s thinking, Mr. Lesiak

at UBS has buy ratings on Agnico-Eagle and another Canadian

company, Goldcorp, in part because the bulk of their revenue

is generated in placid locales. John Hill, a gold analyst

at Citigroup, advises buying Barrick Gold and Newmont Mining.

Mr. Hathaway of Tocqueville Gold also counts

Goldcorp and Gold Fields among his selections. Others include

Ivanhoe Mines, a Canadian company developing a large mine

in Mongolia, and Randgold Resources, which he said is “run

by a very smart group of people in West Africa.”

But he sees many mining companies as poor

investments. “Their main product is going up in price,

and they can’t transfer it to the bottom line,”

he said.

He said he was “beginning to see signs

of intelligence” from a variety of companies on allocating

capital, and predicted that profit margins “should come

out of this funk they’ve been in.” That may make

it more worthwhile to own the stocks than the metal now, but

he stressed that investors should buy mining shares in spite

of what happens in the boardroom, not because of it.

“There is only one reason to buy gold

stocks, and that’s because you think the gold price

is going up,” he said. “It’s not a growth

industry.”