Rare Coins: A Distinct and Attractive Asset Class By Robert

A. Brown, Ph.D., CFA

Dear

Fellow Numismatist and Coin Person,

Every now and then an article

is published related to the subject

of rare coin investing that deserves

a closer look. This is one of those

articles.

I invite questions and dicsussions one

on one afterward.

Abstract

It has been suggested that the decade

ahead may offer relatively unattractive

asset class returns for the most traditional

investment categories such as large-cap

domestic equities. The resulting debate

has promoted interest in such less traditional

asset categories as venture capital,

hedge funds, commodities, timber, real

estate, energy, works of art, and collectibles

on the part of both institutional and

individual investors. It is this last

category of rare collectibles, specifically

coins, which I examine within this paper.

According

to the Financial Times, over the past

50 years art as an investment has shown

returns in line with the S&P 500

Index, according to the Mei/Moses Fine

Art Index, which tracks 6,300 works

sold at auction in New York. From 1954

to the end of 2003, art returned +12.6

percent, according to Mei/Moses (versus

+11.7 percent for the S&P 500).

Under this

broader rare art and collectibles universe,

similarly attractive performance can be

found in the rare-coin market, which,

excluding silver coins and bullion-based

gold, exceeds $40 billion. This paper

offers an unbiased assessment of the inherent,

fundamental, and relatively permanent

risk, return, and diversification properties

of the robust collectables sub-segment

called numismatics and is based on rare-coin

pricing data spanning a 62-year period.

The

data accumulated, analyzed, and presented

here suggests a highly attractive complementary

asset category that even with a small

allocation provides good diversification

for a well-diversified portfolio, and

whose returns look impressive when compared

against the fixed-income category and

as an inflation hedge. In addition,

capital and economic market conditions

suggest that rare coins could exhibit

above-normal returns compared with underperforming

recent years.

Allocation

of a portion of an individual's portfolio

to rare coins must be pursued with full

appreciation for the non-income generating

nature of this asset category and recognition

that no profit-generating corporate

entity stands behind it. Moreover, rare

coins exhibit a relative lack of liquidity

and potentially high transaction costs.

With

the failure of the S&P 500 to reach

lows that would have brought the majority

of fundamental valuation measures back

to their historic norms, many of our

industry's more serious thinkers, those

with real gravitas, have suggested that

we'll experience long-term investment

challenges ahead. Investment luminaries

such as Robert Arnott (editor, Financial

Analysts Journal, Peter Bernstein (consulting

editor, Journal of Portfolio Management),

Bill Gross (PIMCO), John Templeton (Franklin/Templeton),

Bill Bonner (The Daily Reckoning), Jim

Grant (Grant's Interest Rate Observer),

Jeremy Grantham (GMO), and Stephen Roach

(Morgan Stanley) have suggested over

the last two years that the decade ahead

may offer relatively unattractive, if

not painful, asset class returns for

the most traditional and vanilla investment

categories such as large-cap domestic

equities. The resulting industry-wide

debate has prompted a serious reexamination

of less traditional asset categories

such as venture capital (and its associated

neighbors and offspring within the private

investment arena), hedge funds, commodities,

timber, real estate, energy, and rare

art or collectables. It is this last

category of rare collectibles that I

examine within this paper—focusing

specifically on the subcategory of rare

coins or numismatics.

Stephen

Roach, among others, believes that domestic

stocks, bonds, and residential real

estate are simultaneously and significantly

over-valued as a result of excess liquidity

having been pumped into our economy

through actions by the U.S. Federal

Reserve and by the monetary, savings,

and investment behaviors of foreign

nations. If true, as financial planners

we have the responsibility to seek less

traditional asset categories that remain

predominantly unaffected by today's

extreme overabundance of liquidity.

Rare

coins is one such nontraditional asset

category. But why consider rare coins

as a viable component of your client's

total wealth management solution? As

will be demonstrated below, rare coins

have historically offered fairly consistent

and attractive levels of return, risk,

and diversification. Over the last 62

years, this asset category has delivered

an arithmetic mean annual return (before

inflation) of 10.5 percent with a relatively

low standard deviation of 12.3 percent.

But the real benefit derived from this

asset category lies in its diversification

power. Some of its best relative performance

is delivered during those periods when

long-term bonds perform particularly

poorly.

Moreover,

it is not uncommon for high net worth

clients to already be comfortable with

and have significant holdings in the

rare art or rare coin markets. Nevertheless,

investment in the asset category of

rare coins entails a series of distinct

challenges. These potential impediments

include transaction costs (bid/ask spread),

transaction time, specialized knowledge,

proven investment properties, market

depth, lack of dividend or interest

income, and recognition that no profit-generating

corporate entity underlies the asset

category.

Clearly,

rare coins are a highly distinct asset

category, offering a remarkably different

set of investment characteristics and

properties. But the impediments recognized

in the preceding paragraph must be overcome.

Much as with physical real estate (so-called

"bricks and mortar"), the

sale and purchase of rare coins entails

incurring a measurable bid/ask spread.

This obstacle is significant, but with

reduced trading, investors can satisfactorily

overcome turnover through the attractive

long-term fundamental returns accruing

to this asset category. Once again,

just like physical real estate, participants

in the rare coin market should allow

significant time to complete acquisitions

or sales. Nevertheless, the speed with

which coin prices evolve is sufficiently

slow and gradual to accommodate the

more extended time required for transactions.

Finally,

just as with physical real estate, specialized

knowledge is well developed and readily

available at a reasonable cost and is

delivered by a wide range of professional

dealers in the marketplace. The challenge

of verification is no longer an issue,

as all investment quality coins are

authenticated and encapsulated by two

primary service bureaus: Professional

Coin Grading Service and Numismatic

Guaranty Corporation of America. Valuation

is well handled by the ready availability

of recent transaction prices (providing

investors with accurate bid/ask spreads)

and through the advice of professional

dealers—much as is the case with

the private real estate market. Safekeeping

(storage and insurance), however, remains

an ongoing expense—once again,

not dissimilar from bricks-and-mortar

real estate.

The

last two potential impediments—proven

investment properties and market depth,

are the primary subjects of this article.

As described below, returns in both

an absolute standalone basis and, more

importantly, in a well-diversified portfolio

context, have been highly attractive

over the last 62 years. Similarly, the

market for rare coins is deep, well

developed, and improving.

Art

and Collectibles Universe

I begin my examination of rare coins

with a quick high-level review of the

far broader rare art and collectibles

universe. If the investment merits of

rare coins are real and substantive,

then we would expect to find equally

attractive performance within the more

broadly defined arena of art and collectibles.

As reported

in the January 27, 2004, London Financial

Times, the Artprice Global Index rose

1.5 percent in 2003. This index includes

the prices of 30,000 works of art sold

at 2,900 auction houses around the world

in 2003 and is considered to be a reasonable

measure of the state of the aggregate

global high-end collectables marketplace.

In 2004, the Artprice Global Index rose

24.4 percent. Another index, the Mei/Moses

Fine Art Index—All Art, showed

gains of 21.7 percent and 13 percent

in 2003 and 2004, respectively. Over

the last 50 years (1955–2004,

inclusive) this index appreciated 10.5

percent annually versus 10.9 percent

for the S&P 500, 6.6 percent for

10-year U.S. Treasury bonds, and 5.4

percent for short-term U.S. Treasury

bills. This index is noteworthy because

it tracks over 8,000 works sold at auction

and is therefore based on real-time

investor-realized pricing. Fernwood

Art Investments LLC, a New York-based

company, founded recently by former

Merrill Lynch & Co. Inc. veteran

Bruce Taub, began offering art-based

funds in early 2005 as an alternative

asset class. Funds and investment partnerships

are being formed to offer shared interests

in portfolios of paintings by old masters,

impressionists, and others. Fernwood

states "Art is like what real estate

was 30 years ago, it's ripe for investment."

Rare

collectibles as an investment and as

a personal pursuit have been with us

for centuries. But one of the oldest

and most well-developed segments of

the collectables asset category is that

of numismatics or rare coins. In 1912,

the U.S. Congress created the American

Numismatic Association (ANA) to promote

popular interest in the study of numismatics.1

Barry S. Stuppler, a member of the ANA's

nine-person board of governors, estimates

that the total rare coin market experienced

domestic sales approximating $2 billion

in 2003. Moreover, he estimates that

the total supply (market value) of domestic

rare coins is in the neighborhood of

$40 billion (and this figure does not

include bullion-based gold and silver

coins that would bring the total market

value up considerably).

The

depth, vitality, and consistency of

the numismatic marketplace are exemplified

by numerous anecdotes.

In

February 1989, Kidder Peabody launched

a $40 million rare coin investment

fund, later increased to $110 million,

named the American Rare Coin Fund.

A

year later, in February 1990, Merrill

Lynch underwrote a $50 million fund

called the NFA World Coin Fund Limited

Partnership. United Bank of Switzerland

(UBS) maintains a separate and independent

division, UBS Gold & Numismatics,

designed to provide an ultra high

level of professional advice by experienced

experts in the field of numismatics

to its private client base.

In

a July 2002 Sothebys/Stack's auction

a 1933 $20 double-eagle gold piece

sold for $7,590,020. In 1960, this

same piece traded for $25,000—a

14.6 percent annual rate of return

over 42 years.

In

an August 1999 Bowers & Merena

auction, an 1804 proof silver dollar

sold for $4,140,000. In 1960, this

same piece traded for $30,000—representing

a 13.5 percent annual rate of return

over 39 years.

In

an early 2004 Blanchard and Company

auction, a 1913 Liberty nickel sold

for $3 million. In 1960, this same

piece traded for $50,000—a 9.8

percent annual rate of return over

44 years.

Finally,

in a May 1999 Goldberg Coins auction,

a 1907 ultra high-relief $20 double-eagle

gold piece sold for $1,210,000. In

1960, this same piece traded for $20,000—an

11.1 percent annual rate of return

over 39 years.

It should

be emphasized that the returns stated

above are gross of appraisal, insurance,

storage, and other transactions costs

(similar to but higher than what one would

experience in the private real estate

industry).

In the

context of these examples and data,

this paper's objective is to offer an

unbiased assessment of the inherent,

fundamental, and relatively permanent

risk, return, and diversification properties

of the robust collectables sub-segment

called numismatics.

Methodology

Rare coins may be stratified along numerous

dimensions; however, one convenient

classification divides the universe

by metal type: copper, silver, gold,

and other precious metals. The behavior

of the precious metals (gold, platinum,

and palladium) spot and futures markets

has significantly affected the return

behavior of rare gold coins during periods

of extreme precious metals price volatility.

So as not to confuse and otherwise intermix

the behavior of precious metals and

numismatics, I have excluded gold and

other precious metals (platinum and

palladium) coins from this paper's analysis.

Moreover, for consistency and reliability

I have restricted the analysis to U.S.

coins and pricing data has been drawn

exclusively from domestic sources.

All

rare coin pricing data was provided

by the following two sources: Handbook

of United States Coins with Premium

List (the Blue Book) for the annual

copyrights 1942 through 1951, and A

Guide Book Of United States Coins (Red

Book) for 1950 through 2004.2

Coin-price

data provided from these publications

was used to build unique equal-weighted

(by dollar value invested) portfolios

of coins for each individual year. These

portfolios were then tracked to the

subsequent year and an annual return

was calculated. The composition of each

year's portfolio was uniquely tailored

in order to most evenly distribute holdings

across the entire available domestic

universe at that time. Selections were

evenly spread across all copper-based

and silver-based U.S. coins. For publication

copyrights 1942–1960, portfolios

consisted of 600 individual coins. For

copyrights 1960–present, portfolios

consisted of 650 unique rare coins.

The higher 650-coin count was used during

the later years with the objective of

better representing the breadth and

depth of the more modern rare coin market

relative to the somewhat narrower pre-1960

marketplace.

Minimum

coin condition was generally held to

the highest available as reported in

the then-current Whitman publications.

In the initial years, such as 1942,

"fine" was the minimum condition

included within the 600-coin portfolios.

The maximum condition (MS-65) appearing

across all portfolios was similarly

defined by the reporting limits of the

Whitman publications.

As an

example, a portfolio of 650 copper and

silver coins was created and based on

the pricing appearing in the 2004 edition

of A Guide Book of United States Coins.

Coins were selected with the objective

of evenly dispersing the holdings across

the entire available universe as reported

in the 2004 Red Book. Portfolio holdings

were equally weighted (by dollar amount

invested in each coin). The 2005 edition

was used to reprice the original portfolio

and determine an annual rate of return,

(+16.39 percent in this instance.)

A

Critical Question

A critical question concerns the exact

start and end dates for the annual 12-month

investment windows. For example, the

2004 edition has a 2003 copyright and

was first released to the public in

late July 2003. The start date for the

subsequent 12-month investment window

depends on when the coin price data

was collected for this publication.

This paper's analysis is based on a

specific estimate for each annual return's

inception date. The following methodology

was employed to make this estimate.

A series

of 62 annual returns were calculated

based on the Blue Books and Red Books

spanning 1942 through 2004. This series

was compared against annual returns

for 13 other unique and fully differentiated

asset classes (spanning both fixed-income

and equities). The annual rare coin

return series was next shifted one month

at a time, both forward and backward.

This generated a series of 31 alternate

comparisons (that is, no time shift,

1-month through 15 months shifted backward,

and 1-month through 15-months shifted

forward). An evaluation was completed

for each of these 31 return series.

Specifically, I calculated the correlation

coefficients between the rare coin series

and each of the 13 other asset categories.

A median correlation (across the 13

alternate asset categories) was identified

for each of these comparisons. I then

identified the single rare coin time

series (from among the 31 alternate

shifted series) that delivered the highest

median correlation coefficient. The

answer turned out to be the rare coin

series that had its series shifted backward

in time by one month. In other words,

I found that by assuming that pricing

data taken from the 2004 edition of

the Red Book with copyright 2003 was

actually obtained from the marketplace

on November 30, 2002, then the correlation

coefficients with 13 other common asset

categories were maximized. This result,

in effect, amounts to a shift backward

in time by one month (that is, from

December 31, 2002 back to November 30,

2002).

Underlying

this methodology are the following premises.

First, coin prices appearing in a 1990

edition with copyright dated 1989 will

have been collected either very early

in 1989 or sometime in late 1988. Second,

asset classes have a strong and fundamental

tendency to move in tandem with the

passage of significant time. Thus, they

generate positive correlation coefficients.

Third, the most realistic assessment

as to the time positioning of the annual

rare coin series can be determined by

positioning the annual window so as

to achieve a maximum median correlation

coefficient. The statistical result

identifying an initial start date of

November 30th of the year preceding

the annual copyright date is intuitively

appealing. It suggests that the data

reflected in the 1990 edition with copyright

1989 was current and immediate in the

rare coin marketplace as of November

30, 1988. The November 30, 1988, date

is also logically consistent with the

public availability of the final publication—that

is, on or about July 31, 1989. This

would allow approximately eight months

to collect the rare coin data, interpret

it, update the guidebooks, send them

for printing, and distribute them to

retailers for public sale.

Results

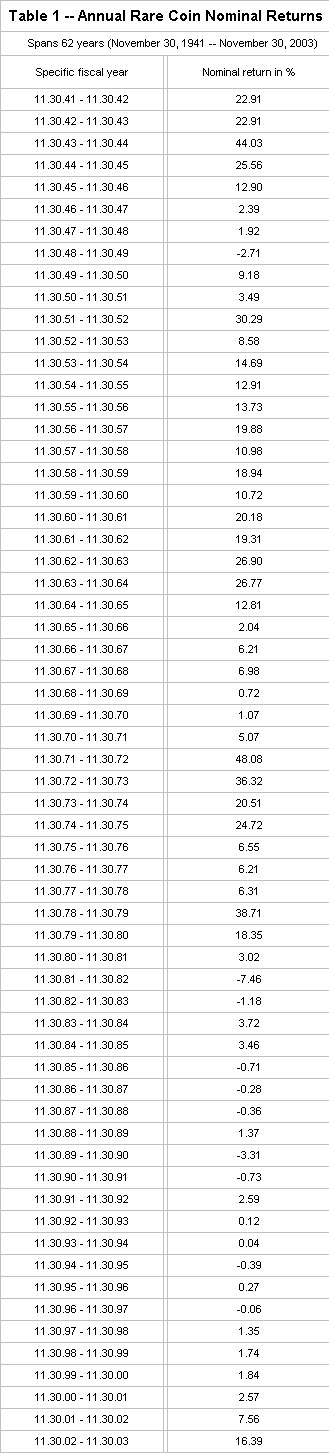

Table 1 provides this paper's estimates

for rare coins' annual returns spanning

the period November 30, 1941, through

November 30, 2003. Returns ranged from

a low of –7.46 percent (1981/1982)

to a high of +48.08 percent (1971/1972),

with a median annual return equal to

+6.26 percent. During the last 62 years,

rare coins delivered a positive return

84 percent of the time (52 of 62 years

as based on annual returns) and an annual

return greater than 10 percent 40 percent

of the time (25 of the years from 1941

through 2003, inclusive).

Table

2 provides the nominal (not inflation-adjusted)

summary statistics for this series.

Relative to 13 other popular asset categories,

rare coins appear to offer relatively

higher average annual returns with commensurate

to moderate levels of return volatility.

Over the last 62 years, rare coins offered

an average annual arithmetic mean return

of 10.46 percent and an average annual

geometric mean return of 9.83 percent,

with a standard deviation of 12.3 percent.

This compares quite favorably against

growth stocks over this same 62-year

period, which delivered average annual

arithmetic and geometric returns of

12.35 percent and 11.02 percent, but

with a significantly higher standard

deviation of 17.1 percent.

It

should be noted that Table 2 reports

on all total return series for which

monthly return data is available spanning

the entire time period indicated (November

30, 1941, through November 30, 2003).

Data for asset classes other than rare

coins were taken from the Ibbotson Associates

databases. Standard deviations were

calculated on annual returns with years

starting and ending on November 30 as

described in the data methodology in

preceding sections of this article.

It is believed that the standard deviations

are directly comparable across all of

the asset classes appearing in Table

2, including rare coins, because each

return series is based on actual transaction

data as opposed to valuation estimates

(as frequently occurs with private real

estate).

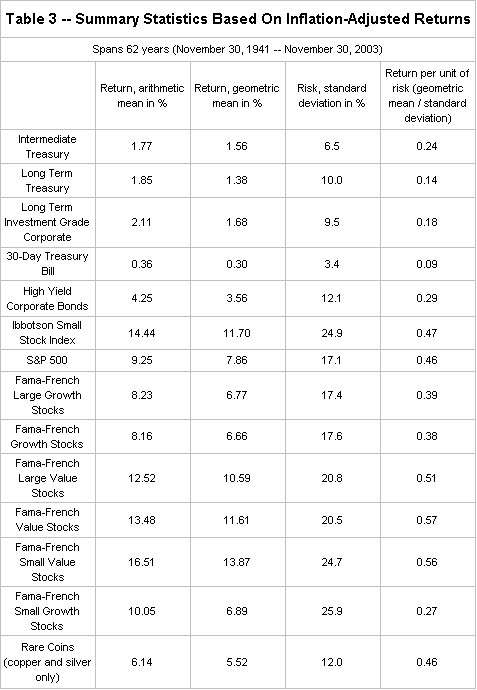

Table

3 provides the same statistics but in

real (fully inflation-adjusted) terms.

A relevant observation for rare coins

is highlighted through a comparison of

Tables 2 and 3. Observe how, after adjustment

for inflation, rare coins' return-per-unit-of-risk

declines from 0.80x to 0.46x. Yet, intermediate

U.S. Treasury bond's return-per-unit-of-risk

declines by a far greater amount, falling

from 0.99x to 0.24x. This difference is

a result of rare coins' propensity to

deliver a degree of protection during

inflationary environments. This observation

is supported by the clearly superior correlation

coefficient between coins and inflation

(0.12) relative to the correlation coefficient

between the S&P 500 and inflation

(–0.31).

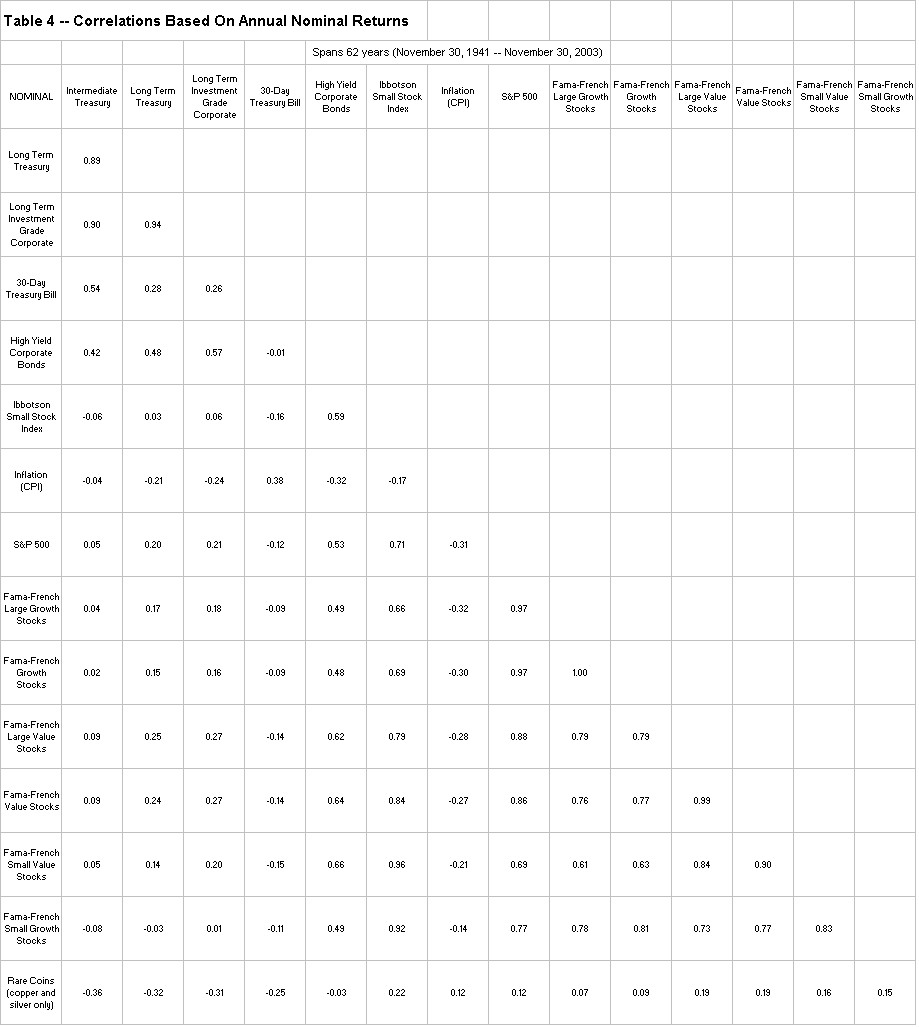

Table

4 reports the correlation coefficients

between rare coins and each of the 13

primary asset categories (plus CPI inflation)

based on nominal returns (non-inflation

adjusted). Rare-coin correlations with

equities tend to be higher than with

fixed income due to fixed income's poor

performance during periods of rising

inflationary expectations. Note rare

coin's correlations of 0.12 and –0.36

with the S&P 500 Index and intermediate

U.S. Treasury bonds, respectively, offering

powerful diversification potentials.

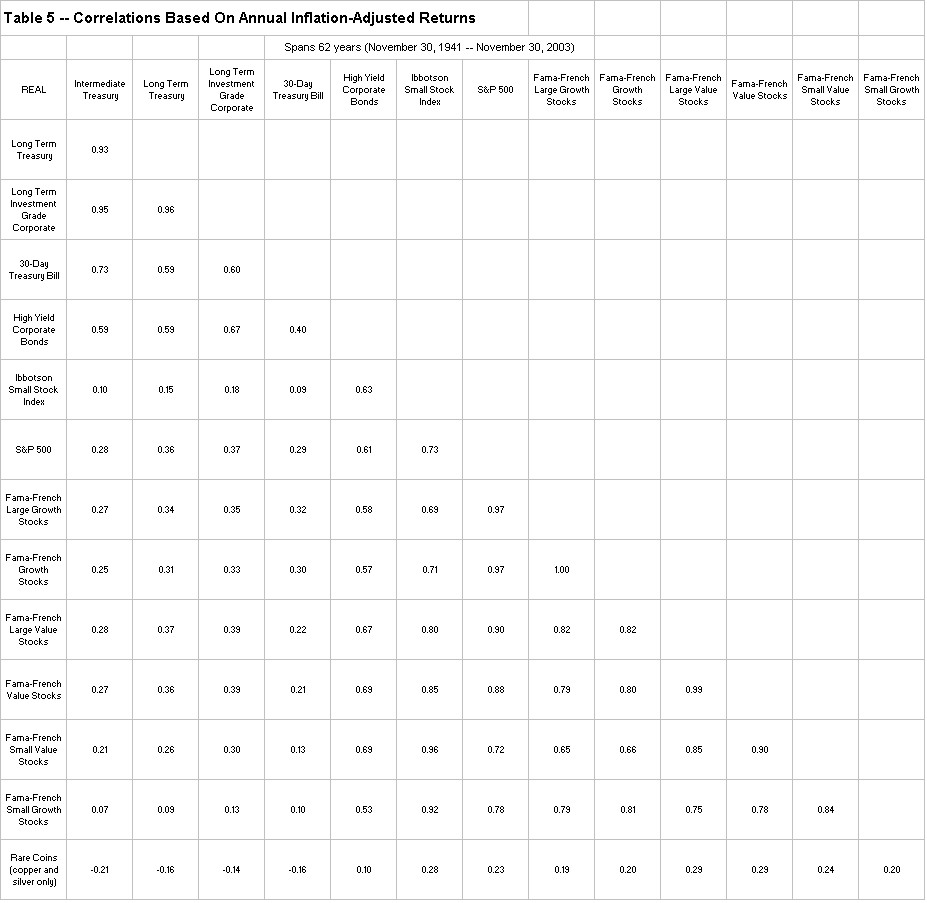

More

Powerful Diversification Role

Using real returns (after adjustment

for consumer price inflation), we obtain

the correlation coefficients appearing

in Table 5. Comparing data appearing

in Tables 4 and 5, we note that correlations

increase significantly across all asset

categories moving from Table 4 to Table

5. But the correlations for rare coins

increase less than any of the other

asset categories (that is, rare coins'

average increase amounts to a lesser

+0.112 versus the other 13 asset categories

average +0.153 increase). This smaller

change results from coins' superior

behavior during inflationary environments

and allows numismatic investments to

potentially play a more powerful diversification

role within a portfolio.

The

practical benefits or attraction of

rare coins as an asset category are

best demonstrated by examining the cross-time

performance characteristics of portfolios

with and without their inclusion. The

bid/ask spread associated with buying

and/or selling numismatic coins tends

to be quite high. In a cross-time portfolio

context, this has an important practical

implication; specifically, regular periodic

rebalancing of one's allocations to

coins in a portfolio is impractical.

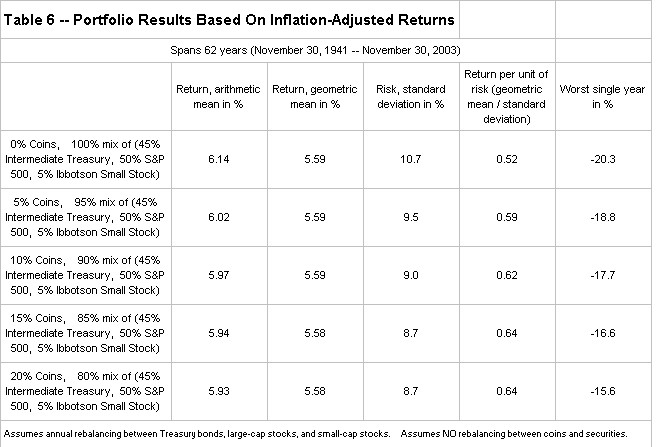

Table

6 provides a historical view of portfolio

performance with and without the inclusion

of rare coins. But this data assumes

an initial allocation to coins of 0

percent, 5 percent, 10 percent, 15 percent,

and 20 percent, with no rebalancing

during the 62 years covered by the analysis.

By avoiding periodic rebalancing, this

paper delivers a more realistic view

of how investors actually construct

and maintain exposure to this attractive

asset category.

Notice

how a portfolio with an initial 15 percent

allocation to rare coins delivers a

geometric mean return 1 basis point

lower than that same portfolio with

a 0 percent allocation to coins. But

the standard deviation falls from 10.7

percent to 8.7 percent after the inclusion

of rare coins, and the worst single

annual return improves from –20.3

percent (without rare coins) to –16.6

percent (after inclusion of rare coins)

But

no asset category should be evaluated

solely on the basis of simple summary

statistics spanning some long-term time

period. Asset categories have a propensity

to deliver performance attuned to the

current-period capital market and economic

environments in which they operate. During

the 18-year period ending November 30,

1999, for example, rare coins returned

an unattractive 0.0 percent a year.

The

causality underlying this painful time

period is not difficult to identify.

First, during the prior 18-year time

period (1963–1981) coins returned

+14.2 percent annually, generating a

level of over-excitement that probably

drove rare coin prices to a transitory

level from which prices needed to fall

back. Second, during the nine years

ending November 30, 1999, the S&P

500 returned +21.01 percent a year.

This abnormally high stock market return

spanning an unusually long time period

had the effect of pulling assets either

out of or away from investment in numismatic

coins. Third, inflation (as measured

by the CPI) was running at a rate of

+12.74 percent for the year ending November

1979. Just seven years later, this same

inflation rate had fallen to +1.29 percent

(year ending November 1986). This remarkable

fall in the rate of inflation removed

a key motivational factor that had previously

been driving coin prices during the

18-year period ending November 30, 1999.

Improving

Coin Environment

Today it would appear that the environment

is changing. Capital market and economic

dynamics are potentially evolving in directions

that will result in below-average stock

market returns while at the same time

delivering a period of rising inflation.

If we experience such a capital market

environment, rare coin investments may

deliver above-average returns.

Graph

1 provides a historical cross-time view

of the path followed by inflation-adjusted

rare coin prices since 1941 plotted

on exponential scale (natural log scale).

By using an exponential scale, equal

vertical distances correspond to identical

percentage rates of return independent

of the current absolute level of coin

prices. The solid line identifies the

growth of one dollar invested in numismatic

coins over the 62-year time period.

This line shows an average annual inflation-adjusted

geometric mean return of 5.5 percent.

The dashed line shows the constant rate

of return path determined by applying

a best-fit analysis. This second, perhaps

more realistic, characterization of

history shows an average annual geometric

inflation-adjusted return of 5.6 percent

for numismatic investments.

Since 1941,

rare coin returns have followed a reasonably

constant return path—exhibiting

occasional periods of out- and under-performance.

But as of November 30, 2003, rare coin

prices stood 131 percent below their trend

line path. This level of below-path pricing

is most likely a function of the recent

below-normal return experience being driven

by low inflation in combination with considerably

above-normal stock market returns. Of

special note, coin returns began a marked

turnaround starting November 30 2001 having

risen a total of +25.2 percent (unannualized)

since that date.

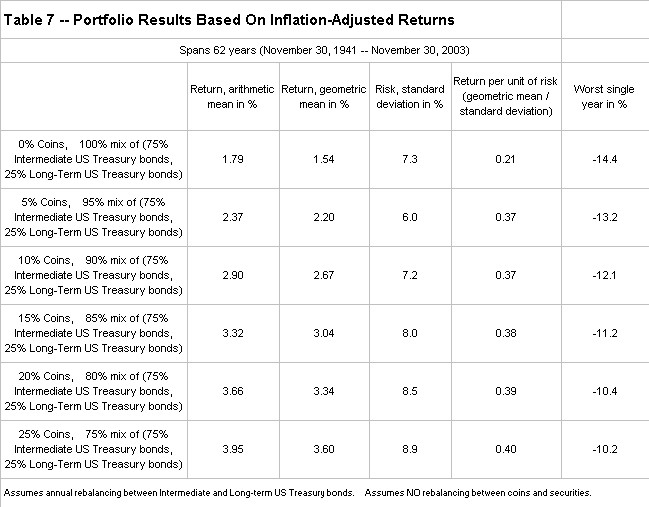

A

different method for exploring the environment-dependent

nature of rare coin returns is demonstrated

by comparing fixed-income portfolios constructed

with and without numismatic investments.

Table 7 shows the 62-year summary statistics

for these alternate fixed-income portfolios

in real terms (that is, after adjustment

for CPI inflation.) By making these comparisons

after inflation adjustment, we are able

to emphasize how relatively small allocations

to rare coins can deliver radical improvements

to a fixed-income portfolio's inflation-fighting

performance.

Table

7 presents a series of six portfolios

with initial allocations to numismatic

investments of 0 percent, 5 percent,

10 percent, 15 percent, 20 percent,

and 25 percent. As before, the allocations

between rare coins and the other asset

categories are not rebalanced with the

passage of time. The fixed-income portion

of these six portfolios consists of

a mixture of long- and intermediate-term

U.S. Treasury bonds which are rebalanced

once each year to maintain a constant-percentage

allocation.

The fixed-income

portfolio without numismatic investments

experiences a standard deviation of 7.3

percent. The same portfolio with an initial

10 percent allocation to rare coins delivers

a lower standard deviation of 7.2 percent

and a higher geometric mean return of

2.67 percent (versus 1.54 percent without

coins). Similarly, note how the bond portfolio

without rare coins suffers a worst single

year of –14.4 percent. In contrast,

the bond portfolio with an initial 25

percent allocation to numismatics experiences

a far less severe worst single year performance

of –10.2 percent. These data suggest

that investors seeking the most conservative

portfolios (that is, bond portfolios)

may be better served by incorporating

small allocations to numismatic investments

as a method to significantly enhance the

inflation-protection characteristics of

their otherwise attractive fixed-income

securities.

Investability

Three issues generally define the question

of just how viable rare coins or numismatics

are as an investable asset category for

small portfolio allocations. These three

factors are the bid/ask spread, liquidity,

and asset class-specific expertise. Bid/ask

spreads in the rare coin arena are consistent

with those found in other sub-segments

of the rare art/collectables marketplace.

At the high end, bid/ask spreads can approach

40 percent. But the rapid growth of both

the electronic and physical auction market

and the robust development of authentication

and grading of rare coins are serving

to reduce these spreads across the numismatic

spectrum. The best-developed, commonly

traded, and standardized (through third-party

authentication) coins may trade at bid/ask

spreads approaching 10 percent.

Liquidity

concerns the time it takes to execute

a transaction, whether a buy or a sell.

It also affects the size of the transaction

and indirectly the bid/ask spread that

is paid. In the field of numismatics,

the transaction time period is properly

measured in months as opposed to minutes

or hours, such as one would find in

trading large-capitalization shares

on the New York Stock Exchange.

In general,

the rare-art marketplace requires significant

knowledge, experience, current information,

and close contacts with key participants

to be fruitfully exploited from an investment

standpoint. The field of numismatics

is no different. But one of the reasons

that a bid/ask spread exists is to compensate

the rare-coin dealer for the advice

and consultation he or she provides.

Yes, part of the bid/ask spread is compensation

for performing the function of, in effect,

marketmaker. But in today's numismatic

market, there exists a wide cross section

of highly professional coin dealers

who view their buyers as long-lived,

permanent clients for whom they deliver

expert advice and consultation on how

best to assemble a portfolio of numismatic

items designed to achieve a long-range

objective. Such dealers have intimate

knowledge of markets and the longevity

of participation to properly assess

the current environment. So as with

many other investment asset categories

such as venture capital, buyout, hedge

funds, and real estate, one pays for

the required (and desired) expertise

via the direct or indirect bid/ask spreads

reflected in the investment vehicle.

Rare coins are no different.

Conclusions

As ANA's governor Barry S. Stuppler has

suggested, the marketplace for numismatics

is both broad and deep, having now reached

an aggregate market value in the vicinity

of $40 billion (and this figure does not

include bullion-based gold and silver

coins that would bring the total market

value up considerably). It is an active

market where single isolated auctions

can experience transaction volume over

$30 million. Professionalism and initial

efforts towards institutionalization have

been demonstrated by numismatic investment

funds launched by Kidder Peabody and Merrill

Lynch and by United Bank of Switzerland's

UBS Gold & Numismatics professional

consulting division.

Pricing

data drawn from the last 62 years of

history (1941–2003) suggest an

attractive and potentially highly complementary

asset category—particularly relative

to fixed-income securities and as an

offset to inflation. Over this period,

rare coins, the S&P 500, and long-term

U.S. Treasury bonds have delivered geometric

mean returns of 5.52 percent, 7.86 percent,

and 1.38 percent, respectively, after

adjustment for inflation. But after

reflecting their differential standard

deviations, we find that rare coins,

the S&P 500, and long-term U.S.

Treasury bonds have delivered return-per-unit-of-risk

of 0.46x, 0.46x, and 0.18x, respectively

after inflation adjustment. Rare coins'

greatest benefit may be one of diversification.

The S&P 500 typically correlates

with other common asset categories at

a level of between 0.28 and 0.97 (inflation

adjusted). In contrast, numismatic investments

have delivered correlations across similar

asset categories ranging from a far

lower –0.21 to 0.29.

Robert

A. Brown, Ph.D., CFA serves as Chairman-Investment

Management Executive Committee and Chief

Investment Officer for GE Private Asset

Management, Inc., located in Encino, California.

Endnotes 1. The American Numismatic

Association (ANA) maintains the distinction

of being one of the very few organizations

in the United States to operate under

a charter. The purpose of the organization,

as stated in its federal charter, is

to advance and promote the study of

coins, paper money, tokens, medals,

and related numismatic items as a means

of recording world history, art, economic

development and social changes, and

to promote greater popular interest

in the field of numismatics. On April

10, 1962, the Congress passed a second

act making the ANA a permanent and perpetual

nonprofit, educational organization.

Today, the ANA maintains a library with

more than 50,000 reference materials

available for loan to members free of

charge.

Handbook of United States Coins with

Premium List was written by R.S. Yeoman,

Lee F. Hewitt, and Charles E. Green.

A Guide Book of United States Coins

was written by R.S. Yeoman and edited

by Kenneth Bressett. Whitman Publishing,

LLC of Atlanta, Georgia, produces both

of these publications. The Handbook

of United States Coins focuses more

on wholesale prices. A Guide Book of

United States Coins focuses primarily

on retail pricing.